Featured

Featured

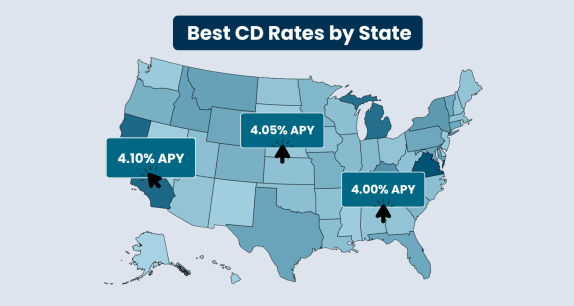

If you’re looking to grow your savings with minimal risk, certificates of deposit (CDs) can be a reliable choice—especially when interest rates are strong. However, with banks and credit unions offering varying APYs depending on location, finding the best rate isn’t always straightforward. The Best CD Rates By State Map helps you quickly compare top […]

Receive exclusive rate alerts and CD offers directly to your inbox.

FI Resources

View All